Trust in the Age of the Shareholder

A cadre of old bald men with three-piece pinstripe suits sat around a mahogany table with brass “scales of justice” in the middle. On the wall behind the man at the head of the table rests a 72 inch by 108 inch canvas of Robert Birmelin’s The Twenty Dollar Bill.

“The Allentown plant has fallen behind again, Mr. Abernathy,” said Martin Veridian in a bold, ambitious tone. Veridian was a forty-two-year-old Director of Operations with hopes of one day succeeding Abernathy, whom he thought both terrifying and incompetent. “The workers are on their seventh straight week of overtime. They are fatigued and I would like to propose a change to shift configuration so they can be refreshed. By hiring another shift, we’ll add to the plant’s labor cost but we will improve safety and quality.”

Abernathy’s odd combination of sharp, bird-like features and old aged flabbiness gave him a large gullet and an unflattering “quadruple chin” that Veridian and his peers often secretly chided him for. Lurched forward like a fat scarecrow and glaring over the tops of his brass reading spectacles, Abernathy quipped, “what will Allentown’s profits be next quarter?”

The executive team viewed Abernathy as a shell of the man he once was. Veridian knew Abernathy’s popularity waned due to industry competition. Other companies were innovating while Abernathy numbly focused on survival. The company was over-leveraged and the only equity financing available was from sharks. Abernathy had taken the company public ten years before but seemingly aged thirty years over this time. The stock price fell steadily for the past three years as dividends dried up and Wall Street pressured him to either spark growth or restructure.

Abernathy was looking for ways to unlock hidden growth and Veridian knew the stars were aligned to get his way. It seemed an obvious tradeoff: sacrifice the earnings already deemed lackluster by Wall Street in exchange for long-term growth. Notwithstanding his present advantage, Veridian hated thinking like a politician. He deeply cared about the well-being of the Allentown employees and wanted the company to survive. Plus, he had the added incentive of future promotion.

Veridian allowed for a short pause to avoid looking desperate. “We actually think we can improve throughput at the plant, which will improve our contribution profits per day by 25% within 18 months. Next quarter our profit margins will go down, though. The plant will produce more, be safer and there will be less risk of product recall risk, but there will be a period where we lose some profitability.”

Veridian knew that Abernathy possessed a high opinion of him and almost always heeded his advice. To his surprise, Veridian’s measured approach was met with an incredulous look. Abernathy collected himself and calmly said, “I am meeting with the bank at 1:30. We are on the cusp of tripping a covenant. I can’t risk the whole company on this move. I apologize, everyone, as I have to get on a conference call. Meeting adjourned.”

Veridian was shocked. He knew about the bank situation, but the workers in Allentown would snap like twigs if they didn’t get some relief. A mistake could literally cost someone a limb, or worse, hurt millions of end users. Veridian tried to chase away the selfish voice whispering to him: if Allentown fails, you will never be CEO and you’ll have to start all over someplace else.

Twenty Years Later

Martin Veridian stood at the floor-to-ceiling window in his new office overlooking PNC Park in downtown Pittsburgh. Gray hair was a charming accompaniment of age that helped Veridian’s executive appearance. He was rather handsome, but he always looked a little too young. He was too busy to exercise seriously, but ate healthily and ran regularly, giving him a slender appearance complemented by a strong jaw line. Bright LED bulbs amply lit the glass fish-bowl style offices which surrounded an ocean of open workspaces. The lights gave the place energy commensurate with Veridian’s style – bright, welcoming, and clean. He was reflecting on the interview with Fortune Magazine at two o’clock.

The recall at the Allentown plant ten years ago was the best thing that could have happened to him, but Veridian would never say that to a journalist. He and a few of his colleagues hired an investment bank while the company was in bankruptcy and led a management buyout.

Veridian’s first order of business was to shut down the Allentown plant, which was at first an unpopular move. The company was hemorrhaging cash and the shutdown made them profitable again almost immediately. The New York Times ran a piece about the company suggesting its new private equity owners were going to “saddle it with debt, enrich themselves with cash, and leave the company gasping for air.” Veridian hoped they wouldn’t do that; he brought them in to save his own career and the company.

He focused on what he could control. He set up a program for the Allentown workers to receive severance and coordinated with Allentown community leaders to help workers find training opportunities for new careers. For those interested, he relocated them to the company’s other four plants around the country.

In his second year as CEO, he aptly steered the business through the dark ages by aligning the company with two disruptive startups through joint ventures. Sure, they gave up value, but it proved to be well-calculated. The JVs allowed the company to ride the wave of technological innovation rather than be overwhelmed. This was met with ire from most of the company’s longer tenured employees, many of whom possessed the technological insight necessary to make the JV work. One such employee of 26 years wrote Veridian an email expressing his disdain for the “young, slick, Silicon Valley hipsters who think a business runs on kombucha and foosball.”

He tried his best to manage both the legacy and contemporary shareholders. He launched a social media campaign called “How We Make It,” showing off the company’s other modern, safe, and ergonomically friendly manufacturing facilities. The videos were narrated by one of the former Allentown employees who was now a shift manager in Buffalo. Lastly, he hired a creative agency to revamp the company’s packaging, putting pictures of real employees on labels with QR codes that would trace product back to its origins. The company’s motto was “Always the best since 1902,” but Veridian changed it to “It Takes a Village,” pointing to the urban environments in older industrial cities that the company helped revitalize.

As the Fortune reporter entered the room, Veridian walked up to her with a warm, confident smile. He knew that trust in the company was restored among customers, shareholders, and the media. He also knew that a single word out of place could undo it all.

Dear Lord, Make Me A Veridian

We have a dangerous tendency to caricature others as extreme avatars. It is easy to imagine presiding over tenuous circumstances with clarity and insight (and strong jawlines like Martin Veridian). It is no small crime to attribute malice or even incompetence when options are limited and conditions harsh. Regardless, we are all felons at large in the age of classes, stockholders, and shareholders.

This story was a fictional encapsulation of events across the dozens of companies I’ve worked with in the past 10 years. The point is to provide a false dichotomy. All readers aspire to be like Veridian and not Abernathy. Strategies similar to those employed by Veridian are everywhere. The question is whether Abernathy was too stupid to implement them or if he was constrained by his circumstances. Sure, Veridian is obviously a deft operator, marketer, and politician, but we’ll never know how he would have managed the company through Abernathy’s situation.

In Abernathy’s case, the company failed to keep up with innovative competition. As a result, the business slipped in profitability which crossed lenders and shareholders. To please them, Abernathy tried to maximize efficiency at the Allentown plant, which led to a recall. Perhaps he should have listened to Veridian, but if he did and tripped a bank covenant, the whole company might have been lost. Furthermore, his prior experience told him that changing shift configuration and hiring dozens of new workers in a plant can be risky.

When Veridian took over, the slate was wiped clean. He had new shareholders who were happy to buy the company with pennies on the dollar. The business had no debt and the Allentown plant was closed. Abernathy was once overheard at a trade show saying he envied Veridian’s situation. Perhaps Veridian was better, or perhaps the only true dichotomy between the two was circumstance. No matter what, both Abernathy and Veridian learned that it was nearly impossible to please all stakeholders.

Shareholders vs. Stakeholders

The Business Roundtable, a group of CEO lobbyists, recently released a document called Statement on the Purpose of a Corporation. Below is my executive summary of its message:

“We haven’t always been nice. We’re really nice now. We are going to be nice to customers by giving them value. We are going to be nice to employees by paying them fairly, giving them good benefits, and giving them opportunities to grow. We are going to be nice and ethical to suppliers. We are going to be nice to communities. We are going to be nice to the environment. We are going to be nice to shareholders in the long-term so we can do innovation, because innovation is nice.”

What is nice? What is value to customers? What is fair pay? What are opportunities to grow? What is ethical treatment of suppliers? What is community support? What is long-term value versus short-term?

Please don’t mistake my sarcasm for cynicism. The Business Roundtable contains the likes of Jeff Bezos (Amazon) and Tim Cook (Apple), and those are just the “A’s.” These are people who face pressures I could never fathom. That said, it is impossible to view such a broad “Statement” , void of specificity, as anything other than political rhetoric.

If you have ever taken a finance course in college or business school, you have heard of NYU professor Aswath Damodaran. He is among the pantheon in finance for his definitive role in how we think about valuing companies. He has a fascinating blog post on this topic called From Shareholder wealth to Stakeholder interests: CEO Capitulation or Empty Doublespeak.

In the post, Damodaran defines stakeholders as investors (also referred to as shareholders), lenders, competitors, employees, customers, vendors, and society at large.

He summarizes five versions of corporatism (I recommend the fulsome article for his deep insight into each):

Cutthroat Corporatism: Maximize investor wealth with other stakeholders in the company going along for the ride.

Crony Corporatism: Maximize investor wealth with government officials benefitting alongside investors.

Managerial Corporatism: Maximize management’s interests because investors have failed to put strong governance in place. Generally, management has “bought” employees with “good enough” compensation. Generally, competitive forces require that other companies be in similar situations. Damodaran says this was true of the post-World War II era.

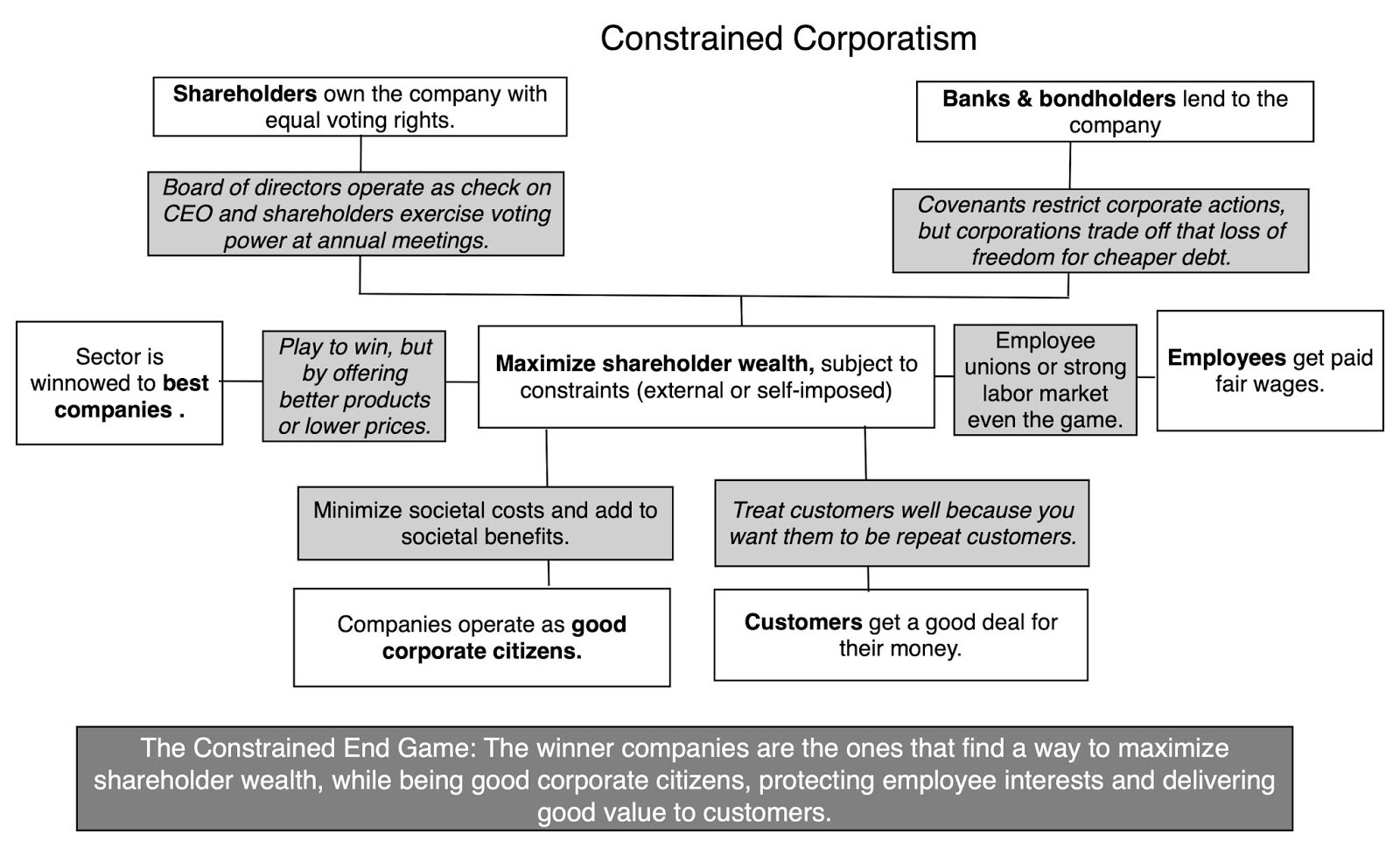

Constrained Corporatism: Maximize shareholder wealth subject to commensurate constraints from other stakeholders (external or self-imposed).

Confused Corporatism: No party is primarily enriched, so management is accountable to no one, and ultimately no one benefits.

He says that while all five models exist, the U.S. primarily adopts either Constrained or Confused Corporatism. Below is a compelling chart he used to illustrate Constrained Corporatism:

Credit: Aswath Damodaran

He suggests that Confused Corporatism may be the worst of all, and gives the example of research universities, with which he is intimately familiar:

“Research universities in the United States are entities built without a central focus, where the stakeholder group being served and the objective is different, depending on who in the university administration you talk to, and when. The end result is not just economically inefficient operations, capable of running a deficit no matter how much tuition is collected, but one where every stakeholder group feels aggrieved; students feel that they pay too much in tuition and have too little say in their education, faculty believe that their rights are being chipped away by no-nothing [sic] administrators and the communities feel disrespected and cheated. If you want publicly traded companies to look like research universities in terms of economic efficiency or taking care of stakeholder group interests, confused capitalism is your answer.”

The post office, among other government run entities, is an example of failure to establish primacy of any stakeholder leading to disgruntled parties across the board.

Lastly, he poses that Constrained Capitalism is only as good as the constraints themselves. Government-imposed constraints may generate short-term satisfaction among some stakeholders, but could put stateside companies at a disadvantage to globalized competition. Self-imposed constraints could satisfy stakeholders so long as someone has primacy. Shareholders are willing to accept less economic benefit in exchange for other benefits, such as an advantage hiring better talent.

Market-driven constraints are best, according to Damodaran. For example, in the food industry, consumers now reject processed foods that were cheaper to make and thus enriching to food company shareholders. Food companies today must harness capitalistic impulses to make natural food or they won’t be able to compete. That only goes so far, however: whether this market constraint is permanent will be decided in the next downturn when people continue to prioritize health to cheap food (side note: this is why I think manufacturing natural food cheaper is the biggest challenge in the industry). As Benjamin Graham wrote, “in the short run, the market is a voting machine but in the long run, it is a weighing machine.”

Trust: The Ultimate Market Force

Along the lines of Damodaran’s constrained capitalism, the July issue of Harvard Business Review published an article called The Trust Crisis, wherein academic and executive duo Sandra Sucher and Shalene Gupta (“S&G”) examine the substance of these constraints: trust. Sucher and Gupta define trust as our willingness to be vulnerable and to believe that others have good intentions toward us. Companies build trust by making promises to stakeholders.

Making promises is easy. Aligning these promises across the divergent interests is the hard part. S&G put it this way:

“Of course expectations can vary within a stakeholder group, leading to ambiguity about what companies need to live up to. Investors are a prime example. Some believe the only duty of a company is to maximize shareholder returns, while others think companies have an obligation to create positive societal effects by employing sound environmental, social, and governance practices.”

Which Side Are You On?

S&G are right, except they forget to leave the door cracked open for nuance. The truth is, most people are stakeholders in multiple ways. To the question of “which do you want?” the nuanced answer is “yes.” I want shareholder, social, environmental and government prosperity.

We hope to retire someday, so hopefully whatever wealth we accumulate grows, or at least doesn’t get lost in the stock market. We hope our kids live in a society with breathable air. We hope other people can be trusted, or else business will be hard and opportunities will dry up. We hope marginalized people can be enriched by this system.

Conclusion: Getting Specific

S&G provide several examples of companies who lost trust and earned it back. It’s always the transparent ones who show their humanity. Dominos Pizza used their formerly awful pizza to become beloved. Japan’s Recruit turned an all-time devastating scandal into an opportunity to create a culture of transparency and to stand out as a company with integrity.

I agree with Damodaran that Constrained Capitalism is the operating system for our economic system; S&G would say that Trust is the code. Constraints are the laws which govern the system. We don’t argue with constraints in the physical world. Gravity is gravity, but with fuel and aerodynamics we can fly. Likewise, constraints may represent rough areas to be made smooth by trust.

As customers, we can vote with our dollar or our time on social media. As suppliers we can choose our customers. As investors, we can choose companies that are antifragile to constraints, or at least robust. We can help those companies identify constraints and work through them. Collectively, all stakeholders can have empathy and recognize that, though I may be a supplier by day, I am a consumer by night and maybe an investor on the weekends. Yes, there are bad actors, but the system will be best served if trust is built. If trust as a currency is devalued, we are in trouble.

Maybe Ben Graham was right. For all the clamoring, activism, and “statements of purpose,” humble and transparent maintenance of trust is the only ways to make the system run. On the receiving end, we vote in the short run with our time, money, and talents. In the long run, our true motives will be weighed and denominated in trust currency. May we not be found wanting.