Biggest Challenge in Food, Part II: Diverging Brands and Manufacturers

In Part 1 of BCIF, we discussed how scaling natural food production is the ultimate challenge in the food space. The inefficiency of (a) subscale/specialty products and (b) natural preservation and higher cost inputs drives the price up, limiting the market. Nevertheless, natural food is in demand. In this round, we’ll discuss a phenomenon seldom discussed: everyone outsources manufacturing.

The challenge? The theory of constraints suggests that every manufacturer should constantly improve by removing bottle necks. One such bottle neck is down-time and changeover. Down-times and changeovers are the result of large variety. In a brand landscape that is now fragmented, outsourced manufacturers who can make a lot of small batches are in high demand. The problem? The cost structure is already expensive, and adding small batches just compounds the problem.

How Did We Get Here?

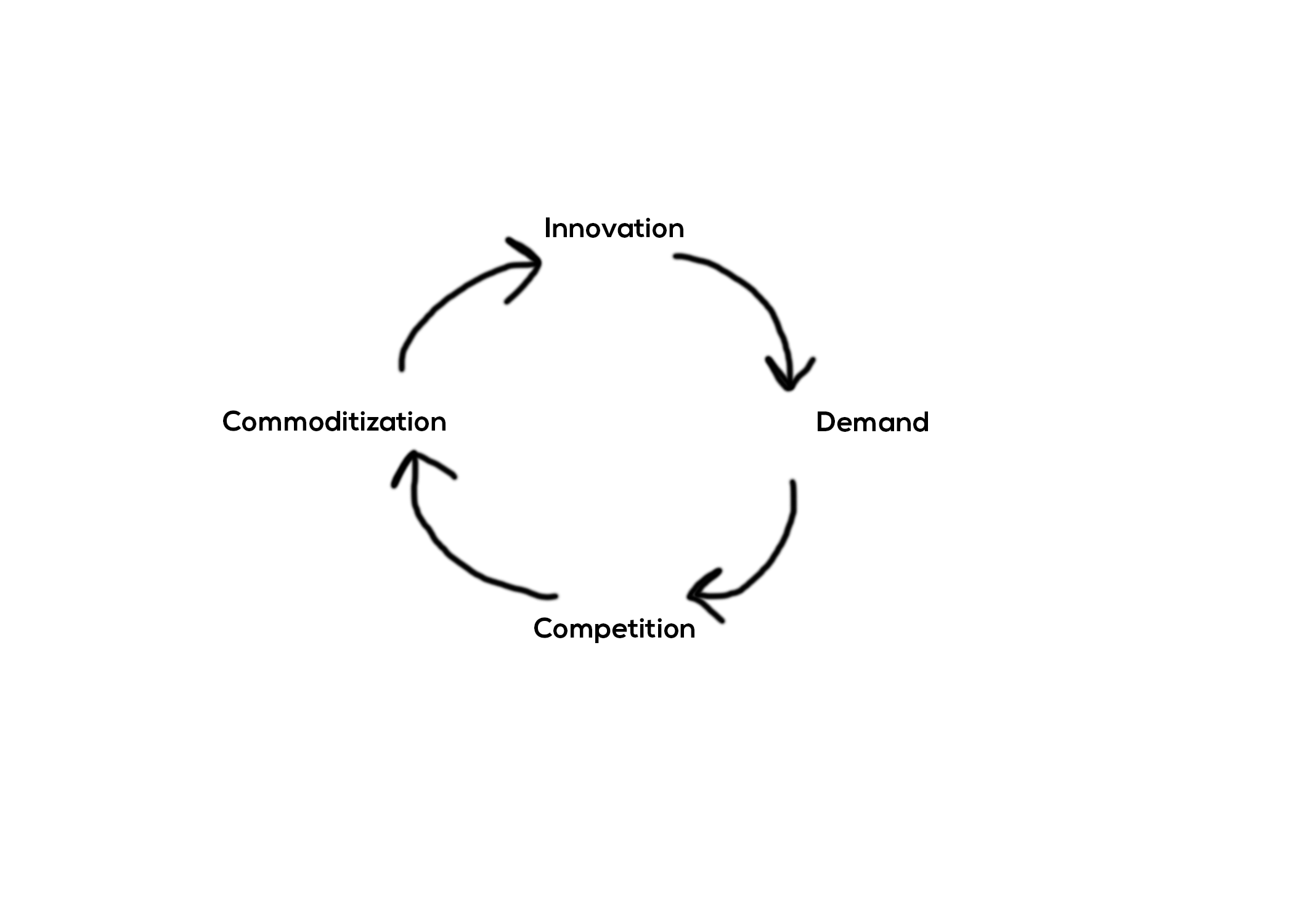

We are fortunate to live in the age of innovation in CPG. For example, twenty-five years ago, plant-based milk, ice cream, and meat alternatives existed but they tasted like garden supplies. Gluten-free products also existed, but many were mistaken either for bird seed or building materials. Today, you may not like them as much as the real thing, but they taste good. It’s easy for anyone to eat a little healthier, because familiar foods comprised of natural ingredients now pervade. This is all part of what I call the CPG Innovation Cycle:

Innovation starts with a creative mind. If the innovator is solving a problem or addressing a consumer need, she must then establish a market for the product. Once established, she has created Demand. As demand grows, it catches the attention of other entrepreneurs and large CPG companies, thus inviting Competition. Once enough competitors have entered the market, the product becomes Commoditized – a race to the bottom to sell product cheapest. The market stays here until innovation crests the horizon like a new dawn. This process is not smooth, however, as each step of the way faces hurdles:

Innovation requires Intellectual Capital – tacit knowledge and deep understanding of the need being solved. Furthermore, it requires technical knowledge, such as understanding the underlying biology, chemistry, and even engineering of a manufacturing system. Demand requires that consumers Adopt and Habituate a product. Remember, we are talking about CPG, so trial isn’t enough. It’s about repeat and lifetime value. Competition can be avoided if there are Moats – structural deterrence to competition. Venture capitalist Jerry Neumann just wrote a must-read article on moats, but in summary, these are barriers faced by competitors in creating and selling similar product. Lastly, the barriers to commoditization are Scale and Capital. This is why the large CPGs often win commoditized categories – no one is going to make canned soda cheaper than the Coke bottling system.

This is not, however, the “Circle of Life.” There are alternative ways to compete that are outside pure commoditization and innovation:

One way to avoid commoditization is Specialization or carving out a subset of a category. Note: this is innovation, but for the sake of terminology, we’ll say that innovation is the creation of a new category, whereas specialization is the incremental addition of features within an existing category. For example, take the jerky business. Until 10-15 years ago, there were a few national brands and the private label stuff in the clear containers at convenience stores. New players came along and created a softer, more tender version, more accessible to some consumers. Other have entered with specialized offerings such as grass-fed beef, different proteins like fish and poultry, and even plant-based offerings. Once these specialties are established, the category is Stratified, meaning divided into smaller chunks.

In jerky, however, the stratified subcategories grew, growing the whole pie. Sometimes, categories stay flat but just get chopped into smaller bits (i.e.: see categories like carbonated soft drink, baking mixes, cereal, etc.). The slowing growth in natural suggests that for all the new innovation, overall categories may not be keeping up. When this happens, each stratified chip off the block gets smaller (hence the smaller dotted line illustrating a series of smaller and smaller cycles):

Out of Sync

Herein lies the great difficulty. We live in the age of micro-innovation. Walk a trade show floor, and you’ll find $1 million revenue brands scrapping it out for differentiation against $5 million brands. It’s common in pitch decks to see competitive matrix slides depicting a startup’s differentiating product features against a half dozen other startups (I’d discourage this approach to both strategy and fundraising in most cases, by the way).

In manufacturing, however, CPG production processes in the last 50 years were built with the Toyota mindset: build A LOT of one thing very quickly and cheaply. In short, manufacturing is stuck in the Commoditization phase, while brands are somewhere between Innovation and Stratification.

For brands, the struggle is to either (a) create new categories through innovation, or (b) add incremental adoption/habituation through stratification that contributes a positive sum to categories. In other words, zero-sum stratification just creates smaller niches and addressable markets. Meanwhile customer acquisition costs are as high as they are in bigger markets, meaning you’ll need to raise the same amount of capital but for a smaller prize.

For manufacturers, the problem is much more rigid. I don’t know how the billions of dollars of online capacity changes its model (see Treehouse’s struggles – a network of scale infrastructure that is impossible to manage given the lack of commonality across assets).

The solution is to move up the curve through specialization and stratification. Historically, co-packers function as excess capacity for large CPG. To survive, you needed speed and efficiency. In small CPG, manufacturing is subject to the same constraints: input costs, overhead, labor, and capital equipment, plus the added challenge of making smaller batches.

This disadvantage can be (and is) becoming an advantage for some. If a small manufacturer can play the range of stratified options in a category but maintain a niche focus, they can take advantage of the demand for artisanal/small-batch processes. They can maintain a modicum of efficiency due to common product characteristics across these products. At Western’s Smokehouse, we make over 1,000 SKUs, but we are rigorous about maximizing throughput across diverse processing and packaging technologies so that our sub-scale customers can benefit from economies of scale.

The key is to lead a niche manufacturing market (maybe $1 billion to $1.5 billion of retail sales). Ultimately, the large players in your competitive set will be prohibited from using their large-scale infrastructure to compete, but the brands and end consumers can still benefit from the scale being created. Move too far from your specialty, and you’ll lose that semblance of scale which makes the economic model work.

To summarize Parts I and II of this series, consumers demand natural food, but it’s expensive because of divergence between manufacturing and brands. Sooner or later, the innovation cycle slows and categories become commoditized, which is we will examine the new age of private label in Part III.