The Biggest Challenge in Food: Naturally Re-Thinking Manufacturing, Part I

Picture yourself preparing a homemade, gourmet meal. You use no preservatives, no chemicals, and no shortcuts toward giving the product the right taste and texture. Now, picture yourself making it for one million people, and they are going to eat your cooking eight months from now.

Welcome to the natural foods industry. It does not scale well. This is the biggest challenge in food: the healthier it is, the closer to its natural form, and the harder it is to produce at scale. No matter, Organic food is now a $48 billion segment growing at 6.3%. Today’s consumer calls for natural, artisanal, authentic, healthful, convenient and delicious (we’ll call all of this “Natural” throughout the article since food’s closeness to nature is its common unifying health attribute).

The consumer is accustomed to blue-box macaroni and cheese price points, all the while transportation, labor, water, and energy costs are all steadily climbing. As for manufacturing itself? Industrial efficiency is maximized at scale. Factories can crank out 15,000 frozen pizzas per minute to deliver a low landed cost a lot easier than they can make your hand-tossed almond flour crepes with organic pomegranate jam and sheep’s milk. The growing demand for natural organic food kicks against the goads of Western industrialized society.

How did we get here?

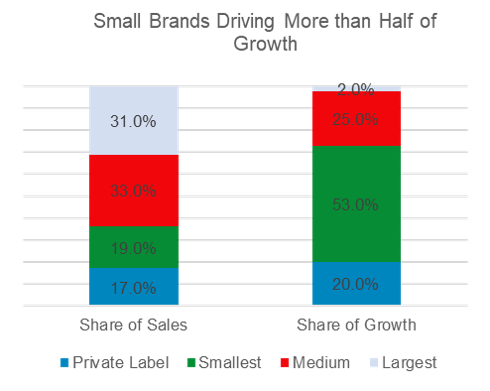

In investment banking and private equity, I spent my career as a meta-participant in the CPG space. From 30,000 feet, I have reviewed pitch decks from hundreds of brands, met as many founders on the annual trade show circuit, and watched myriad panels discuss the existential fate of big CPG brands. Stories of the demise of big CPG at the hands of small brands abound. While 80% of growth now comes from small brands and private label, this, in itself is not the challenge anyone faces.

Nielsen Answers on Demand, Total US, 52 Weeks ending April 15, 2017, pulled from Nielsen article dated June 1, 2017.

The truth is, for every single brand, Natural or not, that has reached a semblance of scale, there are dozens of micro-competitors biting at their ankles. KeVita is joined by an array of kombucha, switchel, and probiotic soda alternatives, to say nothing of the rest of the beverage category that is selling function alongside form (sparkling matcha, ready-to-drink coffee, etc.). My/Mo and Bubbies have built a category in frozen novelties around mochi ice cream out of nowhere that, without a doubt, targets the same calorie-conscious consumer as Halo Top. Essentia faces a bevy of competition from the myriad enhanced water options out there. As I discuss in The Customization of Food, each category has disintegrated into tiny paleo, ancient grained, whole-grain certified, pieces.

What enables fragmented customization? Low barriers to entry. So long as product margins leave enough leftover for sales and marketing, a new entrant can win a micro-beachhead in a small geography. Because it is getting more expensive to acquire the customer’s mind and wallet share (see points 8 and 9 in my Takeaways from Internet Trends, Part I), this approach does not leave sufficient capital to build manufacturing arms. So, they outsource manufacturing to other companies called “Co-Packers.” This wonderful chart from my friends at Cascadia Capital tells the story in the beverage space. There are some categories (such as meat sticks), where co-pack penetration is more like 80%.

Sources: ING, Refresco Company Data, Cascadia Capital

We must ask ourselves whether our industrialized manufacturing landscape is designed for making these products. The new Marketers are, by definition, niche businesses - smaller businesses - which need smaller manufacturing operations. They need manufacturers capable of excellence and efficiency in small batches. Herein lies the paradox: we need subscale manufacturers… at scale.

The Manufacturing Landscape

Manufacturing in an industrial society is a positive feedback loop, fashionably referred to as a flywheel. Manufacturing centers around low input costs, buying power, long run times, and economies of scale. This creates better quality, safety, and pricing. This, in turn, attracts more utilization, which lowers costs, improves quality, enables longer runs, etc. Natural food undoes the flywheel. So why don’t food manufacturers simply pivot?

For the past half century, CPG brands were built on iconic ubiquity. Products like Coca-Cola, Tide, Budweiser, and Hershey thrived on the ubiquity of single SKUs. A SKU is a product, defined by flavor, size, and packaging format - the six-pack of Budweiser, the Hershey bar, the can of Coke. These companies built scaled manufacturing operations around large SKUs and outsourced manufacturing operations for small SKUs.

This approach made sense: when you can run 125,000 Snickers Bars per minute, round the clock, keep that in-house and capture all the margin. When you want to put complementary, specialty products in the market, hire someone else to do that so you don’t disrupt the constant flow of your big SKUs. Batch Processing 101.

While some outsourced manufacturing infrastructure has been built for these smaller runs, the industry is not very straightforward. Most of these co-packers are simply large regional brands with excess capacity. Their co-packing business is usually borderline unwanted, living alternately between wealth and leanness, depending upon whether the co-pack products they made became successful (and ultimately brought back in-house by the large CPGs). They do not really want to be in this business, so they do not make great partners for emerging brands.

The Investment Opportunity

The greatest challenge in CPG is that natural food does not scale well, and this is exacerbated by our industrial manufacturing landscape. Innovation and technology is needed in modular, small-batch, highly flexible manufacturing operations. At Charis Consumer Partners, we are looking for manufacturers with this capability. Generally, they are small, family-owned and excellent within their domain. Sometimes, they own their own brands, and sometimes they are pure co-packers. The future of the industry is in their hands.

Furthermore, we think a major opportunity lies in store brands, or what we call “private label,” which refers to brands owned by retailers (e.g.: Costco’s Kirkland Signature, Kroger’s Simple Truth, Giant Eagle’s Nature’s Basket, Trader Joe’s, etc.). These are also trending toward Natural, and the manufacturing challenges they face are the same as the brands. In fact, they usually rely on Natural brands to supply their Natural private label products. Thus, while private label is a phenomenon at retail, it faces the same challenges as the rest of CPG. We think this is perhaps the most interesting growth area in food going forward, and we’ll discuss this more in Part II.

To conclude, while you sip your organic fair-trade orange mandrake sparkling matcha with collagen and turmeric, thank God that you have the means to buy single serve beverages for $3.95 each, and look forward to the day when it will be more affordable.